Over the past month, much has been written about the real estate slump in Vancouver—particularly in the condo market. The industry is understandably concerned. When sales are over 25% below the 10-year average, everyone—from agents to developers—is taking a pay cut.

While a perfect storm of factors has led to this downturn, much of it is by design.

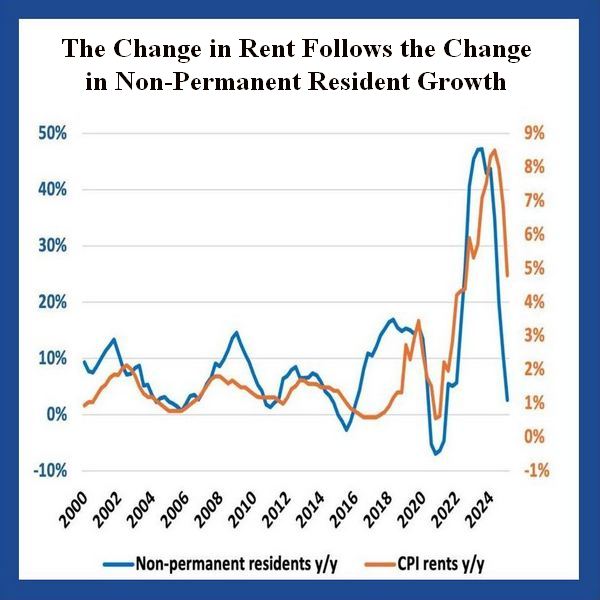

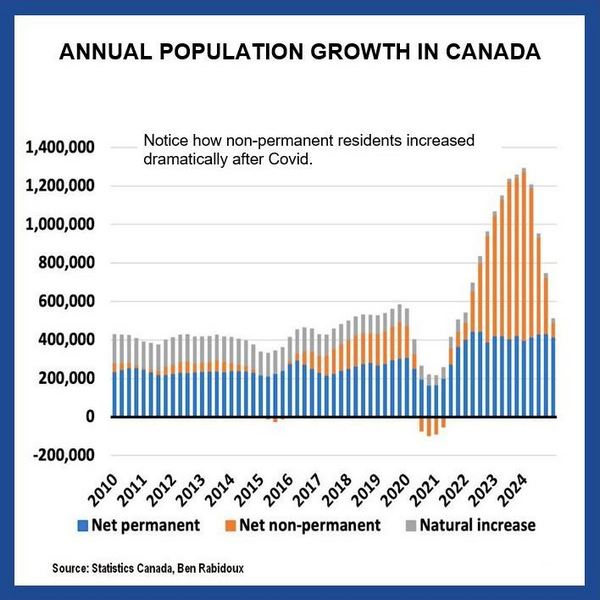

In an effort to improve housing affordability, several policies were introduced: the foreign buyers ban, stricter short-term rental regulations, and reduced immigration levels. It’s basic Economics 101. Foreign buyers and investors represent purchasing groups that often outbid local workers. Removing one and significantly restricting the other has effectively reduced a large portion of demand. Immigration cuts have had a twofold effect. Fewer permanent residents mean fewer homebuyers. Fewer temporary residents mean less rental demand. This helps explain the softening rental market, which in turn makes rental units a less attractive investment.

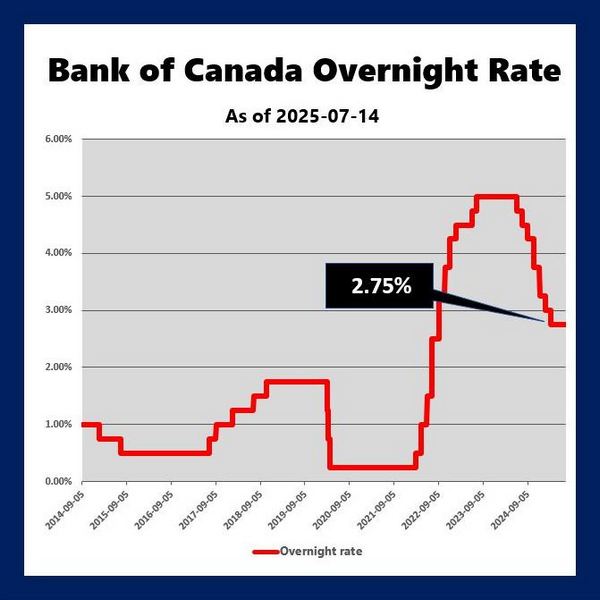

Although interest rates have fallen from their peak, they remain far above pandemic-era lows. The Bank of Canada’s overnight rate reached as low as 0.25% during COVID, peaked at 5%, and now sits at 2.75%. Higher rates not only raise mortgage costs for buyers but also increase financing costs for developers. Add to that economic uncertainty from the U.S. and a softening job market, and it’s clear why the broader real estate market is dragging.

Condos—particularly high-rises—face a unique problem. Their long development timelines make it hard to match supply with demand. It can take six years from the moment a project is conceived to when tenants move in. Many of the buildings currently coming online were planned before the foreign buyers ban, short-term rental crackdown, and immigration changes. As a result, they often contain units that are now mismatched for today’s market: too expensive for local buyers, or designed for short-term tenants (e.g., no parking, very small layouts).

The supply of high-rise condos is increasing just as demand is waning—a classic case of oversupply at the wrong time.

So what’s next?

The government could reverse some of the policies affecting foreign buyers, short-term rentals, and immigration. But doing so would conflict with its stated goal of making housing more affordable. While the government shouldn’t back track, it is not stopping special interest groups from trying.

Interest rates could be lowered to ease mortgage burdens and reduce developers’ financing costs. But interest rates are tied to many aspects of the broader economy. At present, the Bank of Canada remains more focused on fighting inflation than supporting the housing market. A rate cut aimed purely at helping real estate seems unlikely.

This creates a dilemma: if the government steps in to prop up the real estate sector, housing costs will likely remain high. If it doesn’t, a major component of Canada’s GDP—real estate accounts for about 13%—is at risk.

Recent policy changes, like raising the ceiling for CMHC insurance and reintroducing 30-year amortizations for insured mortgages, suggest the government is trying to gently reignite demand. We may be too reliant on real estate to let the market correct on its own.

So expect some policies designed to stimulate interest in the housing sector in the months ahead. But I don’t expect them to significantly boost sales or lift prices—at least not this year.