Recently, BMO published a report stating that the S&P/TSX outperformed Canadian real estate over the past 20 years. According to the report, the TSX achieved an average annualized return of over 7.9%, compared to 5.7% for real estate in an average inflation environment of 2.2%.

While the article implies that equities might be the better option based on recent price movements, focusing solely on recent returns is a bad investment strategy. You need to look at the big picture. Long term.

The report used an average of all residential real estate across Canada, encompassing cities like Vancouver and Toronto, but also smaller towns like 100 Mile House and Spuzzum. Since you cannot buy this “average house”, you need to look at the historical return of the specific area you are considering for purchase.

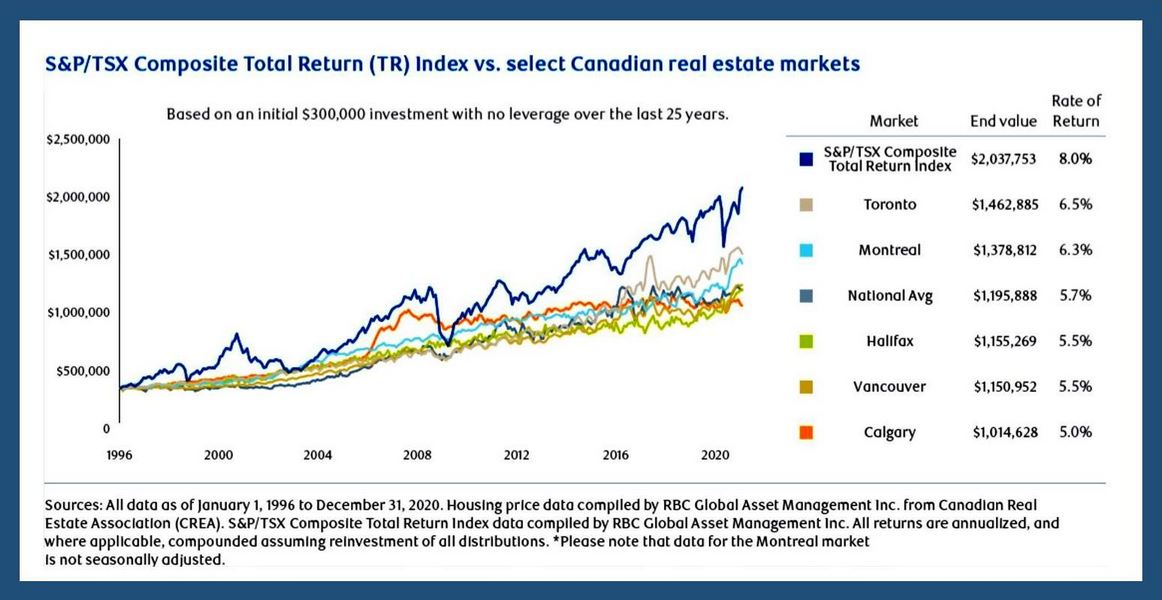

In 2020, an analysis of returns over the past 25 years showed that the S&P/TSX return and the average real estate return have remained relatively stable. Vancouver’s return over the last 25 years was only 5.5%, but even if it were 5%, it wouldn’t matter. The reason? Leverage.

You can buy a $500,000 property with a $25,000 down payment, or 5%. No one can purchase $500,000 worth of Microsoft shares with a 5% down payment. Even if it were possible, the volatility would be intolerable. If the stock price dropped 5%, the equity position of your portfolio would go to zero. The brokerage would require more money immediately to maintain that 5% position, or they would sell your position, solidifying the loss.

Between December 6, 2021, and October 31, 2022, Microsoft shares dropped 35%. If you could buy those shares with a 5% down payment like a house, you would have lost $150,000 on paper if you bought $500,000 worth of stocks. But you would need to come up with $166,250 to prevent the brokerage from selling your Microsoft shares. This doesn’t happen with a house, allowing you to ride out the ups and downs. After 25 years or so, you will have it all paid off, providing an asset that can generate monthly rental income indefinitely.

Also, because you only put down 5%—which is 20x leverage—your 5% return is actually 100% [See the illustration]. And if this property is your principal residence, there is no capital gains tax. For equities, the inclusion rate is 50% of the first $250,000. That is, if you made $100,000, you would add $50,000 to your annual income to calculate your income tax.

There are many ways to argue for equities over real estate but rate of return is not one of them. While it might be entertaining to write an article raising doubts about real estate investment versus equities, in reality with the leverage and tax advantage of a principal residence, there is no comparison.