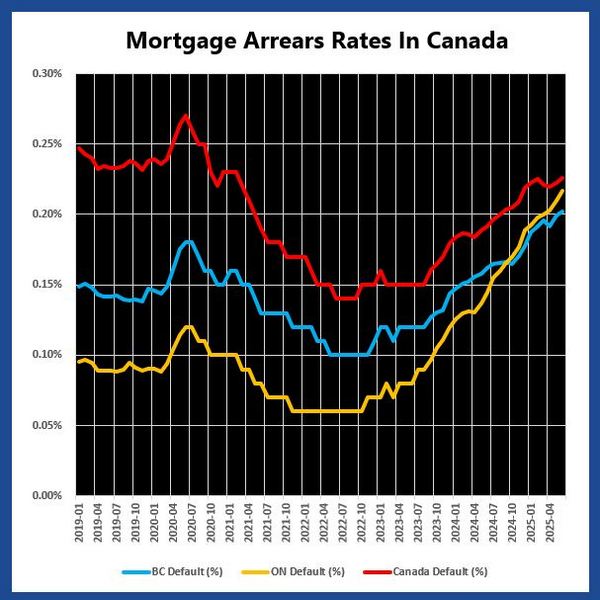

As we see economic conditions worsen, such as increased credit card arrears and mortgage payment arrears, we should check our own finances to see if we need to take pre-emptive action. While it may feel less painful to stick our heads in the sand and avoid taking a hard look at reality, when reality forces you to face it, it will be too late.

The first step is to make sure your income covers all your expenses. Ideally, you should also be saving a little each month—but then again, ideally I’d be eating a well-balanced diet and working out a couple of hours a day. Do the best you can.

Trouble arises when you’re covering some of your monthly expenses with credit cards. This is the first warning sign. Take a close look at your spending and see if there are things you can cut, even temporarily. Then see if you can increase your income, whether through overtime or a side gig.

If you still can’t balance the budget and you own a property, one option is to refinance your home. That means going to the bank and taking out a larger mortgage to cover your debt. This usually makes financial sense since mortgage rates are typically much lower than other types of debt. I recently saw a credit card notice saying the interest rate was going from 20% up to 23% or even 25%. How are they not making enough at 20%?! Argh! But I digress.

Refinancing can reduce your monthly payments—and sometimes by a lot. But it’s tempting to spend the extra cash, and that’s not the best strategy. When you swap out 20% credit card debt for a 5% mortgage, you save money, but remember: you’ve just stretched that debt out over 25 years (or whatever your amortization is). The smart move is to use your savings to pay down the extra mortgage amount as quickly as possible.

But what if your bank or mortgage broker says you don’t qualify for refinancing, and instead offers a private mortgage or “equity loan” for debt consolidation? Should you take it? Whether you actually save money depends on the details. The monthly payment may be lower—and that’s what the broker will emphasize—but once you factor in broker fees, lender fees, and legal costs, you may not come out ahead. In this situation, the only reason to proceed is if you’re about to start missing payments. Missing payments will wreck your credit and push you deeper into the financial doom loop.

That’s why it’s important to look at your finances early: the further along you are in the process, the fewer good options you’ll have. Banks love to lend you money when you already have plenty. Not so much when you don’t.

Give me a shout if you need help with any of this.