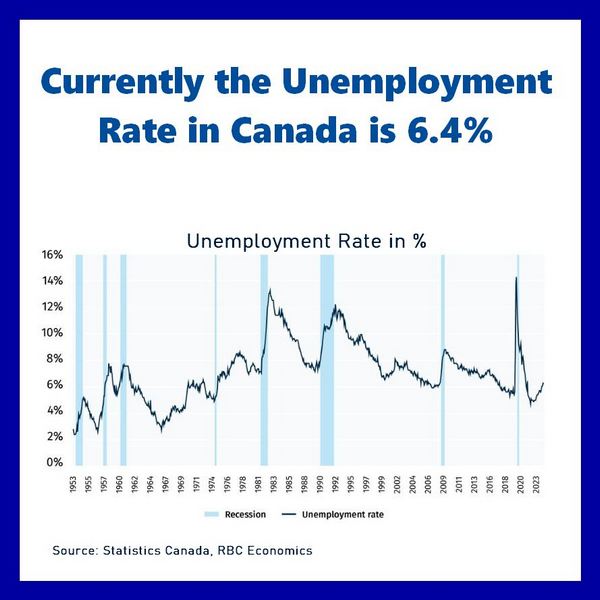

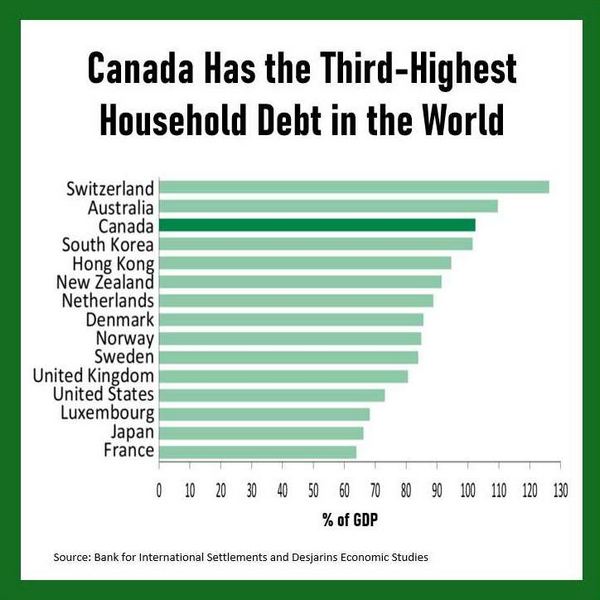

The Canadian economy is weakening, and that’s why interest rates are being lowered. While this may be good news for homeowners hoping for a break on their variable-rate mortgage payments, it’s adding financial pressure for many. Canada is already one of the most indebted countries in the world and the rise in unemployment is making matters worse

Although part of the unemployment increase can be attributed to more people entering the job market, the fact remains that more individuals are losing their jobs.

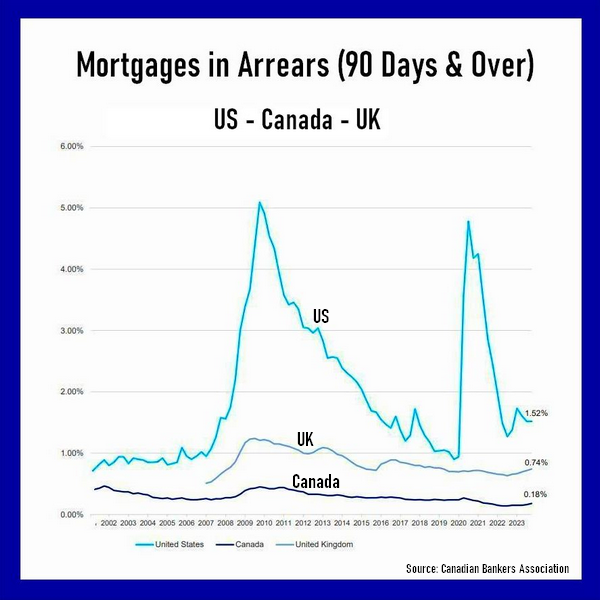

Despite alarming headlines about rising credit delinquencies, the actual numbers remain low compared to other countries and our own historical standards. This may not pose a serious threat to the overall economy, but for those affected, it’s a personal crisis. Unmanaged debt can quickly erode your financial well-being, so addressing it early makes it more manageable.

The first step is to review your spending and cut unnecessary expenses. Next, explore additional sources of income, whether it’s taking on a part-time job or other opportunities. If you own a home with some equity built up, there’s an additional option: consolidating your debt by refinancing your mortgage. Reach out to a mortgage broker to help you assess the options. They can compare the potential benefits of paying a penalty to get a new mortgage versus taking on a second mortgage. Keep in mind, to qualify for refinancing, you’ll need sufficient income and a healthy credit score.

This underscores the importance of acting sooner rather than later when managing your finances. By the time you’ve maxed out credit cards or started missing payments, your credit score may be too low to qualify for low-rate borrowing. Debt consolidation can help reduce interest costs,